The power of banks in four cities: Chicago, D.C., New York and San Francisco

Think a bank needs to be global to be signficant? Community banks control billions of dollars across cities.

There are several ways to assess power, and most of them boil down to who’s got the most money, and/or who’s got the most people supporting them (who collectively have money).

Banks publicly report how much money people deposit in their bank (in the form of checking, savings, CDs, and money market accounts), and how many accounts they have.

So let’s take a look at the banks in each of four metropolitan areas -- the Chicago metro, the New York City metro, the San Francisco metro, and the Washington DC metro -- and the sum of money people choose to deposit with them.

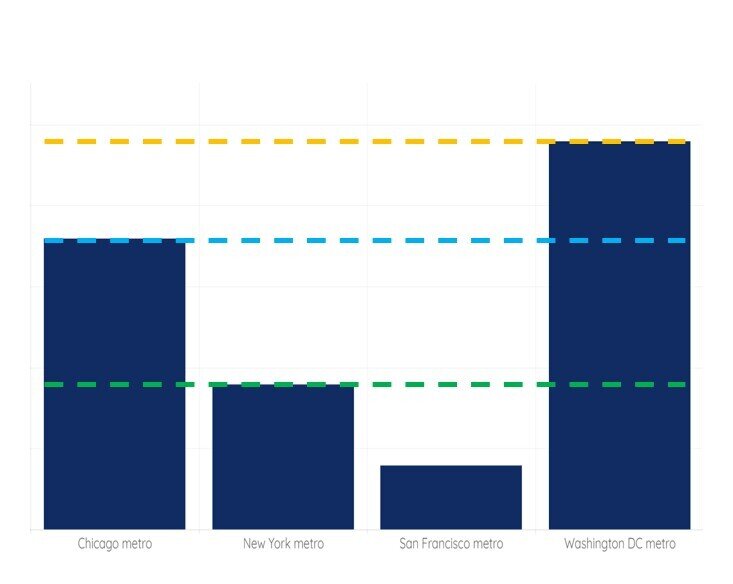

There’s a lot of money in deposit accounts in New York City bank branches.

Bank branches in the New York City metropolitan area have more money in deposit accounts than in all of the bank branches in the Chicago, San Francisco, and the Washington DC metro areas combined.

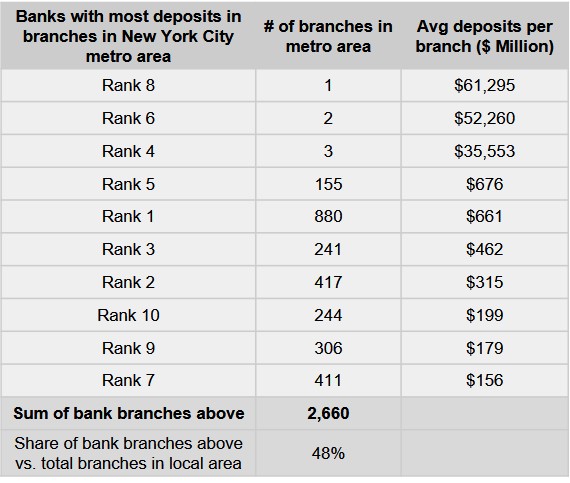

The New York City metro area has 201 banks -- about 10 banks for every 100,000 residents -- with $1.8 trillion put in deposit accounts within NYC area branches. This is $89,000 in bank deposits, per capita.

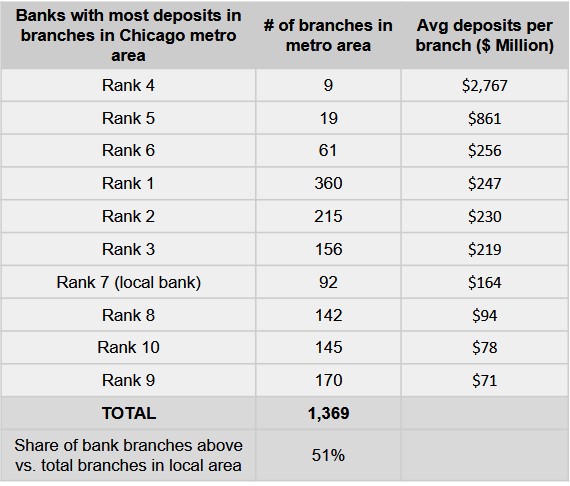

The next closest city with the most banks and money in them is Chicago. There are 189 different banks in the Chicago metro area. This is 20 banks or so for every 100,000 residents, more banks per capita than the other cities on our list. People collectively hold $398 billion in checking, savings, CD and money market accounts within Chicago area bank branches. This is about $42,000 for every Chicago resident.

Chicago has more banks per capita.

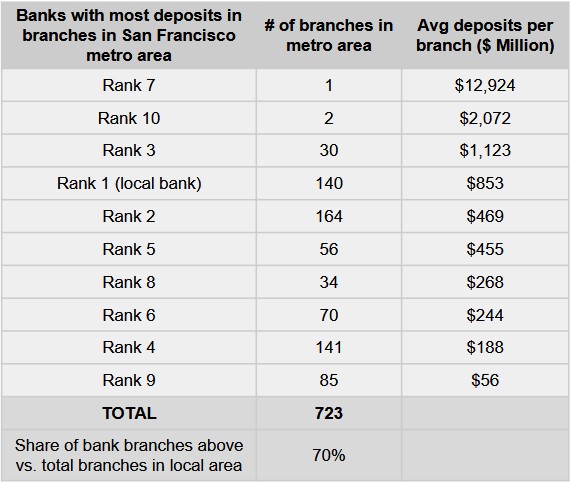

San Francisco bank branches have more money in their deposit accounts per capita than those in Chicago or DC. People living in the San Francisco metro area have about 15 banks per 100,000 people, or 69 total banks. There is about $79,000 in checking, savings, CD, and money market accounts in bank branches in the San Francisco area, per capita.

In the Washington DC metro area, 77 banks -- about 13 for every 100,000 residents -- held $256 billion on deposit in bank branches: about $41,000 per capita.

Money in deposit accounts can come from people and organizations near and far.

The money in any given city’s network of banks can come from people and businesses located across the country, and not just from those residing in the city.

For example, let’s say you live in Seattle. If you bank with a bank solely located in Chicago, your money is in Chicago. If you bank with a national bank, your money may be wherever in the country the bank has an office and chooses to put your money, whether that be Seattle or New York City or Sioux Falls, South Dakota. If you bank with an online bank, chances are the online part of the business is a digital storefront to a brick-and-mortar bank that manages the deposit part of the business, and your money’s at work in the place(s) where that bank works.

The geographic location of a bank’s deposits is important, because banks generally finance communities proportionate to where they have branches and the amount of deposits in them. (There’s something called the Community Reinvestment Act that encourages banks to do just this.)

So take a look at where a bank concentrates its deposits to have some context about where and how a bank is focusing its financing.

(Pro tip: If you want your money to support a particular community, browse banks that have their deposits concentrated there.)

For example: Southern Bancorp accepts deposits from across the country. Because banks generally finance communities proportionate to where they have branches and the amount of deposits in them, Southern focuses the majority of its community financing in the Mississippi Delta.

A few banks dominate in major metropolitan markets.

Of all of the money that lands in deposit accounts in Chicago, 22% is deposited with JP Morgan Chase. That’s a sizeable amount of money from people and businesses in a city controlled by a single bank.

But not as much as New York City, where Chase also controls more money than any other bank in the metro, with 32% of deposits, locally.

In San Francisco, it’s a similar story to New York, but this time, headlined by a different bank: Bank of America controls 32% of money on deposit in San Francisco bank branches.

In the Washington DC metro, E*TRADE Bank controls 17% of deposits.

Among 200 or so banks in each the Chicago and New York City metropolitan areas, JP Morgan Chase has in its Chicago and New York City area branches nearly a fourth and a third, respectively, of all the money in deposit accounts in all of the bank branches in those cities. Bank of America has in its San Francisco area branches a third of all the money in deposit accounts in San Francisco area branches. E-Trade Bank has 17% of all of the money in deposit accounts in the Washington DC area.

Millions of accounts are kept with local banks, the most populous type of bank.

Despite the dominance of the expected market players -- national banks -- in major cities, local banks are meaningful contenders for deposit dollars. (For the purpose of this blog, we’ll define local banks as those that are 100% located within the metro area.)

About 1.9 million accounts are with local banks in the Chicago area. In the New York City area, about 2.6 million accounts are with local banks. There are more than half a million accounts with local banks in the San Francisco area, and over 800,000 with local banks in the DC area.

Local banks have a larger market share in Chicago and DC areas than they do in NYC and San Francisco areas. All collectively control billions of dollars in each market.

Local banks in the Chicago area control 18% of the money in checking, savings, CD and money market accounts in all bank branches across the Chicago metro area.

In the New York City area, local banks control 9% of total deposits in the area.

In the San Francisco area, local banks control 4% of total area deposits.

And in DC, local banks are entrusted with a larger share of deposit dollars than local banks in other cities on our list, with 24% of all deposit dollars .

If these numbers seem modest, remember the amount of dollars on the table: 9% of the $1.8 trillion in deposit accounts in the New York City area is $162 billion; 4% of the $371 billion in deposit accounts in the San Francisco area is is nearly $15 billion.

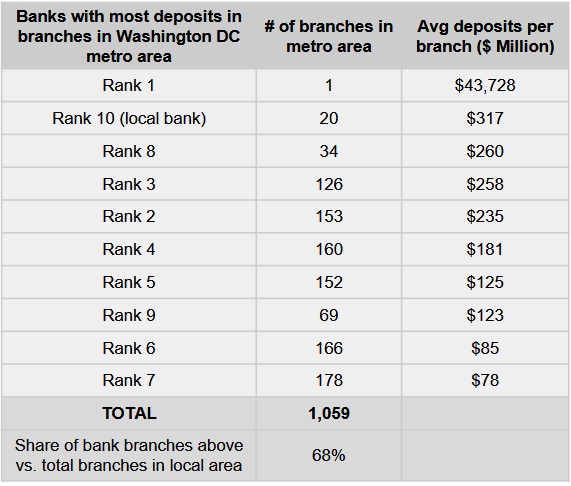

A bank no longer needs to have a lot of branches to have a lot of deposits.

Taking a look at the ten banks with the most deposits in each metro area, you’ll see that a bank need not have many branches to have a leading share of local deposits.

Bank branches, no doubt, may have mattered in helping a bank become popular in the past. Back in the day, when you had to walk into a branch to do your banking, a bank with a lot of branches was able to attract a large customer base. Today, having a lot of branches in key locations across a city is great advertising, above all else. (Bank branches are an expensive sort of billboard for banks. We say billboard, because many people don’t really walk into bank branches anymore. Rather than cash machines, bank branches are more like the Apple Store, or the Nike store, or any other store that still has a storefront. The storefront helps you remember it’s there. With lots of local locations, a bank might lead you to think it’s locally focused. Though as outlined above, a better indicator of local focus is not the number of branches a bank has, but where the bank concentrates its deposits.)

When finding a bank these days, what's relevant to look at is not necessarily how many branches it has, but whether the bank offers a value proposition that matters to you (like financing Native American equity, or small business in Chicago, or small farms in the Mississippi Delta, or sustainability) and the technology to make banking from anywhere possible (like online account opening and mobile deposits).

In Chicago and New York, about 50% of the bank branches you bump into are likely to be owned by one of the ten most popular banks. In San Francisco and Washington DC, there’s closer to a 70% chance that any given bank branch you see belongs to one of the ten most popular banks in those cities. This is great advertising. No wonder these banks are top of mind.

Looking for banks online versus on any given street would likely result in a different set of banks making up the most popular banks in a city for people’s deposits.

Where do you bank, and why?

What banks do you support, and why? What’s your money up to?

Mighty helps you find the best banks for your money and values. Browse banks now.

*Deposit data from June 30th, 2018